The Importance of an Emergency Fund Throughout Life Stages

Understanding the Value of an Emergency Fund

Life’s unpredictability can sometimes be overwhelming. People often find themselves faced with unplanned expenses, such as medical emergencies, job losses, or urgent home repairs. To weather these storms, one of the most prudent financial strategies is to maintain a robust emergency fund.

Consider the benefits of having an emergency fund:

- Peace of Mind: With an emergency fund, you can relax knowing that you have financial resources to cover unexpected costs. This assurance can significantly reduce anxiety about the future, allowing you to focus on your daily responsibilities and long-term goals.

- Financial Stability: Having readily available cash means you are less likely to resort to high-interest loans or credit cards when sudden expenses arise. For instance, the average credit card interest rate in the United States hovers around 20%, which can quickly lead to insurmountable debt if unexpected costs are not managed wisely.

- Flexibility: An emergency fund gives you the freedom to make crucial life choices. Whether it’s resigning from a job you find unfulfilling or investing in a new opportunity, knowing that you have a safety net to fall back on can empower you to take calculated risks without immediate financial concerns.

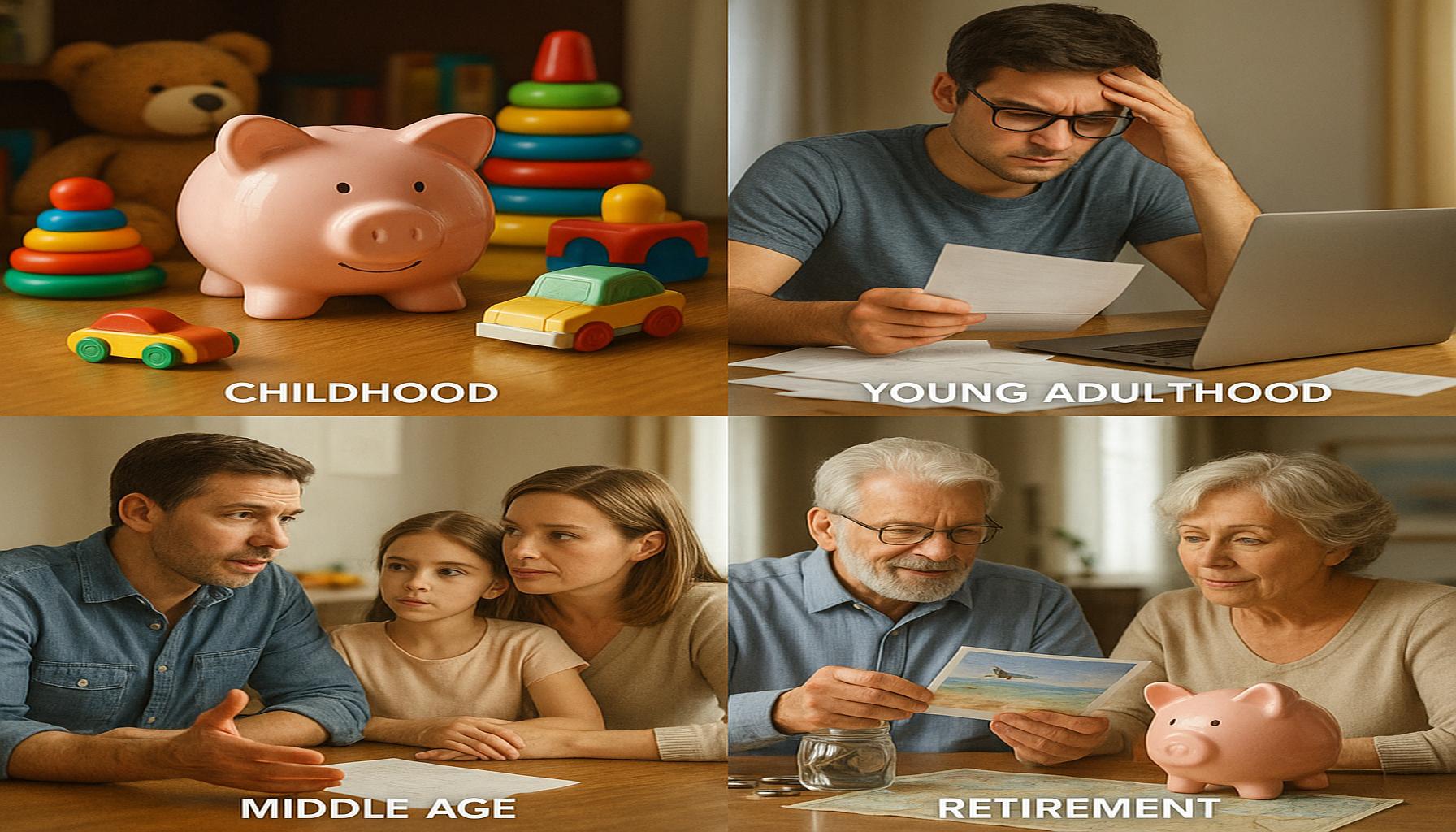

No matter your life stage, the significance of an emergency fund remains undiminished. For instance, young adults embarking on their careers encounter numerous financial challenges, including student loan repayments. They might suddenly face car repairs, medical expenses, or other unforeseen costs, all of which demand financial resources that they may not have saved up yet.

In contrast, parents with children often find themselves grappling with unexpected childcare expenses or urgent home repairs that require immediate attention. As families grow, so too do the complexities of financial planning, making an emergency fund even more essential.

As individuals advance in age, the nature of emergencies may evolve. Older adults may confront health-related issues or unexpected home maintenance needs as they approach retirement. Yet, the fundamental principle of financial preparedness remains unchanged. Regardless of whether you are a recent graduate, a busy parent, or nearing retirement, an emergency fund serves as an essential tool for safeguarding your financial future.

One guideline many financial experts suggest is to aim for three to six months’ worth of living expenses in an easily accessible account. This prepares you to handle life’s uncertainties without sacrificing your long-term financial goals. With an emergency fund in place, you’re not just setting aside money; you are actively protecting your future and ensuring that you remain resilient against unforeseen challenges.

LEARN MORE: Click here to discover how to apply for an Oportun loan

Navigating Early Adulthood: The Foundation of Financial Security

For many, the journey toward financial independence begins in early adulthood. This critical stage often comes with a series of firsts: first job, first apartment, and often, the first taste of financial responsibility. However, it also brings unique financial challenges that can catch many young adults off guard. Issues such as managing student loan repayment, sustaining living expenses, and handling unexpected costs require thoughtful preparation.

Establishing an emergency fund during this pivotal stage can truly set the tone for future financial well-being. Imagine being faced with a sudden car repair or an essential medical bill—without savings, these costs can quickly spiral into a financial crisis. For instance, a survey conducted by Bankrate found that 28% of Americans do not have enough savings to cover a $500 unexpected expense. This statistic highlights the vulnerability many young adults experience when they lack a financial cushion.

Furthermore, the age of digital finance introduces additional risks. With easier access to credit cards and loans, young adults may find themselves swept up in a cycle of debt. A reliable emergency fund helps to mitigate this risk by providing an immediate alternative to high-interest borrowing, fostering healthier financial habits. This principle is particularly resonant given that the average credit card interest rate in the United States exceeds 20%, often leading individuals into a debt trap that becomes increasingly difficult to escape.

Growing Families: The Essential Support System

As individuals transition into family life, the importance of an emergency fund magnifies significantly. Parents must navigate the complexities of financial planning that come with raising children—each developmental stage often brings new expenses. From childcare costs to unexpected medical bills during flu season, the financial landscape quickly shifts and becomes more demanding. Statistics show that the average cost of raising a child to age 18 in the United States is approximately $233,610, which does not even account for college expenses.

Amidst these financial obligations, families can encounter urgent situations, such as home repairs due to unforeseen damage or sudden job loss. According to the U.S. Bureau of Labor Statistics, approximately 3.8 million people experienced job separations in the past year. Having an emergency fund can significantly ease the stress of these situations, allowing families to maintain stability and comfort—even in the face of financial uncertainty.

- Unexpected Health Emergencies: Children can get sick unexpectedly, leading to medical expenses that can deplete savings.

- Emergency Home Repairs: Issues such as plumbing failures or roof leaks can occur at any time and can be costly to fix.

- Job Loss: The prospect of an unexpected job loss can be daunting, emphasizing the need for a financial safety net.

By establishing an emergency fund early on, families reinforce their financial resilience, ensuring they are equipped to handle life’s curveballs without derailing their long-term financial health. As seen throughout various life stages, the role of an emergency fund is more than just a savings account; it becomes a vital part of a financial strategy that promotes stability and peace of mind.

DISCOVER MORE: Click here to uncover the power of compound interest

Building for the Future: The Transition to Midlife

As individuals progress to midlife, typically marked by greater career stability and often increased earning potential, the financial landscape undergoes substantial transformation. However, this period is not devoid of its challenges. Many find themselves balancing a delicate financial dance between supporting children, caring for aging parents, and planning for retirement—sometimes known as the “sandwich generation.” This reality reinforces the critical nature of having an emergency fund, not only to handle immediate concerns but also to secure long-term financial stability.

During this stage, life’s unpredictability brings about more significant financial implications. For instance, according to the Federal Reserve, nearly 40% of Americans would struggle to cover an unexpected $400 expense without relying on credit cards or loans. Midlife often comes with unexpected health-related expenses for both parents and children, which can amplify financial strain. The rising costs of healthcare and insurance premiums can rapidly eat into a family’s budget, making an emergency fund essential for navigating these expenses without jeopardizing other financial goals.

Investing in Stability: Home Ownership and Education Costs

This life stage often sees many families cementing their finances through home ownership. Home repairs—whether a leaky roof or issues with foundational integrity—can happen unexpectedly, leading to costly repairs. The National Association of Home Builders reports that the average homeowner spends about 1% to 4% of their home’s value annually on upkeep and repairs. Without an emergency fund, such costs can lead to unmanageable debt or the need to dip into critical savings meant for education or retirement.

Moreover, as children approach college age, families face a new financial hurdle: educational expenses. The College Board reported that for the 2021-2022 academic year, the average annual cost of attending a public four-year college was around $27,330. In contrast, private institutions average about $55,800 per year when including living expenses. This financial burden is compounded when families do not account for other child-related expenses, such as extracurricular activities and potential medical needs during this hectic stage.

- Home Repairs: Sudden costs for home maintenance can disrupt financial planning and savings goals.

- Educational Expenses: Preparing for college can lead to mounting costs that challenge even the best-laid financial plans.

- Caring for Aging Parents: Long-term care costs can be substantial, calling for a robust emergency fund for peace of mind.

In the context of midlife, the importance of an emergency fund transcends being merely a safety net; it’s a stabilizing factor that encourages proactive financial behavior. Families that have prioritized saving an emergency fund often find themselves better equipped to handle the unexpected without forsaking other financial aspirations. This strategic financial buffer becomes a cornerstone in the architecture of a solid financial future, enabling individuals to pursue goals with confidence, knowing they are cushioned against life’s unpredictable nature.

DISCOVER MORE: Click here to get started on your financial journey

Conclusion: The Lifelong Necessity of an Emergency Fund

Throughout the various stages of life, from young adulthood to midlife and beyond, the significance of establishing an emergency fund cannot be overstated. As we navigate through different challenges, such as student loans, unexpected medical expenses, home repairs, and the financial obligations of raising children or caring for aging parents, an emergency fund acts as a crucial safety net. In fact, studies reveal that approximately 60% of Americans report anxiety about their financial security, underscoring the need for a buffer against life’s uncertainties.

An emergency fund fosters financial resilience, allowing individuals and families to respond to urgent situations without resorting to high-interest debt options. Effective financial planning must acknowledge that expenses can arise at any moment; thus, prioritizing an emergency fund should be a foundational tactic in anyone’s financial strategy. Research indicates that ideally, one should aim to save three to six months’ worth of living expenses in an accessible account—this amount provides a robust framework for securing one’s financial health.

Moreover, as our life goals evolve—whether that involves buying a home, furthering education, or enjoying retirement—it is imperative to regularly reassess and adjust our savings accordingly. Embracing the practice of maintaining an emergency fund fosters a sense of stability and peace of mind, empowering individuals to seize opportunities rather than fear setbacks. Therefore, the journey to financial wellness not only requires prudent spending and investment but also a firm commitment to building and sustaining an emergency fund throughout all life stages. By doing so, we best equip ourselves for whatever the future may hold, transforming unpredictability into manageable challenges.

Beatriz

Beatriz Johnson is a seasoned financial analyst and writer with a passion for simplifying the complexities of economics and finance. With over a decade of experience in the industry, she specializes in topics like personal finance, investment strategies, and global economic trends. Through her work on our website, Beatriz empowers readers to make informed financial decisions and stay ahead in the ever-changing economic landscape.